January 15, 2026

Group insurance models, like Rent Guarantee Insurance (RGI), are helping affordable housing providers address rising eviction rates and insurance costs. These programs cover rent gaps caused by temporary income loss, preventing evictions and maintaining housing stability. For instance, Minneapolis' Beyond Backgrounds program saw a low 1.3% claim rate while supporting over 200 renters between 2018 and 2020.

Key issues faced by affordable housing providers include:

Group insurance models, such as shared risk pools and captive insurance companies, offer a solution. These models stabilize costs, reduce discrimination, and reward good property maintenance. For example, the Housing Partnership Insurance Exchange (HPIEx) insures over 100,000 units and provides predictable premiums and potential financial returns.

Public-private partnerships and government-backed initiatives, like New York's Insurance Law § 3462, further support affordable housing providers by regulating discriminatory practices and offering financial relief. Programs like Rent Guarantee Insurance also reduce eviction risks by covering short-term rent gaps, benefiting both landlords and tenants.

Platforms like Walnut Insurance simplify the adoption of group insurance by integrating solutions directly into housing providers’ systems. With customizable coverage and fast claim processing, these tools help providers manage rising costs while keeping tenants housed.

Bottom line: Group insurance models and targeted government policies are essential for combating the challenges of rising costs, discrimination, and tenant displacement in affordable housing.

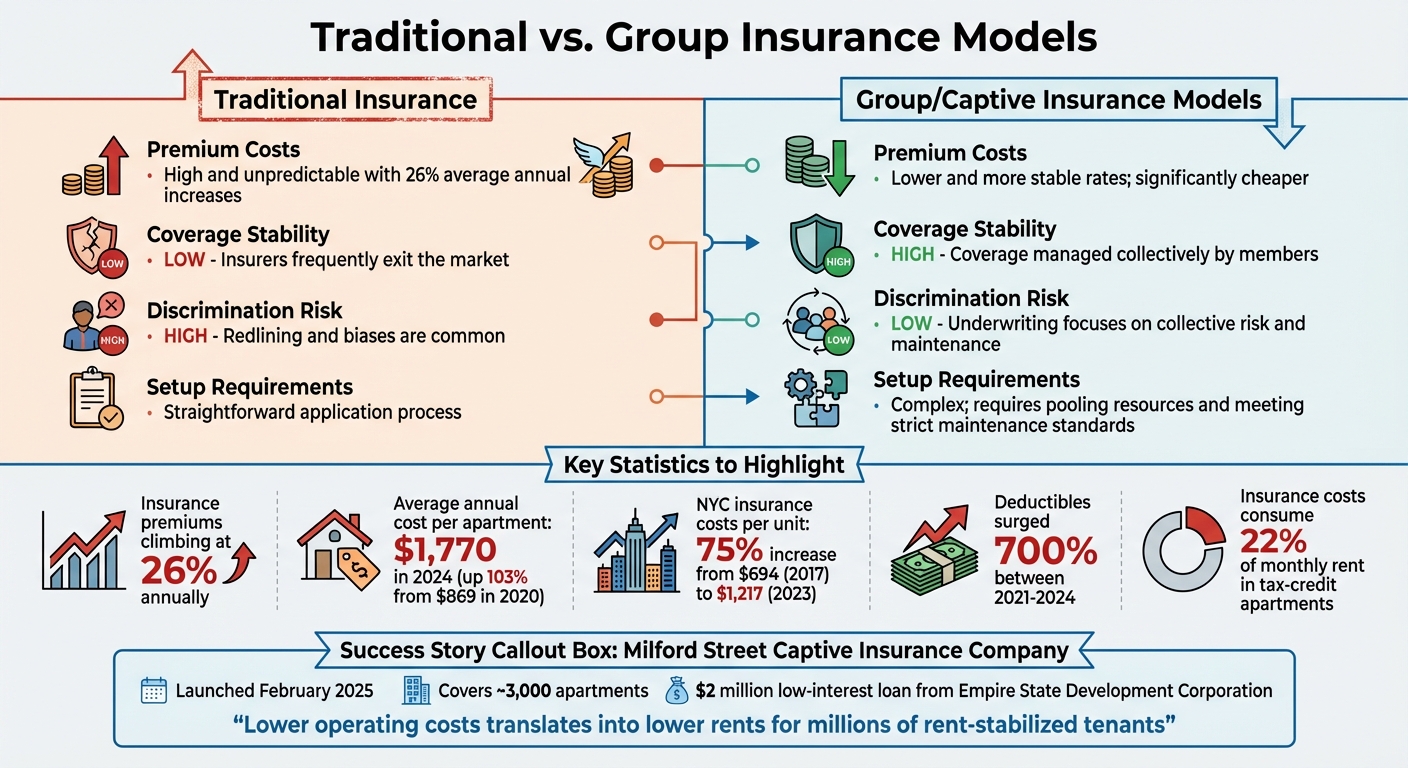

Traditional vs Group Insurance Models for Affordable Housing Comparison

Affordable housing providers are grappling with skyrocketing insurance costs that are stretching their budgets thin. Insurance premiums are climbing at an average rate of 26% annually [7], far outpacing both inflation and revenue growth. By 2024, the average annual cost to insure an affordable apartment hit $1,770 - a staggering 103% jump from $869 just four years earlier [7].

In New York City, the numbers are equally alarming. Between 2017 and 2023, insurance costs per unit surged by 75%, rising from $694 to $1,217. In the Bronx, costs climbed even higher, reaching $1,478 per unit by 2023 [8]. For tenants in tax-credit apartments, this translates into insurance costs consuming 22% of their monthly rent [7].

Adding to the financial strain is an unsettling trend of discrimination. Insurers often refuse to cover buildings that house Section 8 voucher holders or formerly homeless individuals [6][7]. Geographic redlining is another hurdle, with some insurers declining to cover properties in urban areas like New York City or the Bronx [7].

These escalating costs and discriminatory practices are creating financial challenges that directly affect building maintenance and tenant safety.

Unlike private landlords who can increase rents to offset rising costs, affordable housing providers are bound by strict rent caps enforced by government regulations [8]. This creates a financial bottleneck, forcing providers to absorb rising insurance premiums without generating additional revenue.

The ripple effect of these financial pressures is alarming. To manage costs, providers often defer critical maintenance, creating what some experts call a "doom loop." John Crotty of Workforce Housing Group explains:

"If you don't have the money for repairs, a $10 problem can become a $50 problem if you ignore it long enough. And a $50 problem can become a $500 problem if you ignore that longer. This 'doom loop' is unsustainable" [8].

Deferred maintenance leads to deteriorating living conditions, which can ultimately displace tenants. Patrick Boyle, Senior Director at Enterprise Community Partners, highlights the broader impact:

"Ultimately, what these rising operational costs mean is that a greater subset of the affordable housing stock in New York is in financial distress" [8].

To make matters worse, average deductibles have surged by 700% between 2021 and 2024 [10]. These mounting costs and operational challenges underscore the urgent need for alternative insurance solutions.

Affordable housing providers are increasingly exploring alternative insurance models to mitigate these challenges. A closer look at traditional insurance versus group or captive insurance models reveals why this shift is gaining traction:

Comparison: Traditional vs. Group/Captive Insurance Models

| Feature | Traditional Insurance | Group/Captive Insurance Models |

|---|---|---|

| Premium Costs | High and unpredictable; 26% average annual increases [7] | Lower and more stable rates; often significantly cheaper [8] |

| Coverage Stability | Low; insurers frequently exit the market [7] | High; coverage is managed collectively by members [8] |

| Discrimination Risk | High; redlining and other biases are common [7] | Low; underwriting focuses on collective risk and maintenance [8] |

| Setup Requirements | Straightforward application process | Complex; requires pooling resources and meeting strict maintenance standards [8] |

One success story is the Milford Street Captive Insurance Company, launched in February 2025. This collective, formed by seven major landlord companies in New York City, secured a $2 million low-interest loan from the Empire State Development Corporation to establish a self-insurance pool. Currently covering around 3,000 apartments, the initiative is already making an impact. Board member Ruben Diaz Jr. emphasized its importance:

"Lower operating costs translates into lower rents for millions of rent-stabilized tenants" [8].

This model demonstrates how collective efforts can help affordable housing providers navigate a challenging insurance landscape while easing financial burdens for tenants.

Group insurance models allow housing providers to take charge of their insurance coverage. Instead of relying on commercial insurers - who can unexpectedly hike rates or cancel policies - providers pool their resources to form group insurance programs. These programs typically operate as either captive insurance companies or shared risk pools. Below, we’ll explore how each model works and the advantages they offer.

A captive insurance company is essentially an insurance firm owned and operated by its members, created specifically to cover their needs. A prime example is the Housing Partnership Insurance Exchange (HPIEx). Established in 2004 by nonprofit housing developers, this member-owned entity now serves 23 organizations and insures over 100,000 housing units worth more than $27 billion. HPIEx provides coverage for property, casualty, workers' compensation, and health insurance, supporting members with a combined payroll exceeding $150 million [11].

One key benefit of captives like HPIEx is predictable premiums. Members get premium estimates four months before renewal, which helps with stable budgeting. Even better, when the group has a strong year with fewer claims, members receive dividend payments - turning what would normally be a pure cost into a potential financial return. This system not only stabilizes housing costs but also creates a sense of shared accountability.

Captives also promote fairness through individual underwriting and peer benchmarking. Each property is assessed based on its specific characteristics and compared to similar buildings in the group. This encourages members to maintain their properties well, as good performance is rewarded [11].

Shared risk pools, on the other hand, take a simpler approach. Multiple housing providers contribute to a common fund that covers losses across all participants. Unlike captive insurance companies, these pools spread risk broadly, ensuring that a single large claim doesn’t overwhelm one organization’s budget. Most pools maintain a reserve of 10%-20% to handle claims [1].

What sets shared risk pools apart is their ability to offer tailored coverage for industry-specific risks that traditional insurers often avoid or overcharge for. For instance, they provide solutions like LIHTC (Low-Income Housing Tax Credit) recapture bonds, which protect against tax credit penalties during ownership changes, and specialized liability coverage for risks such as “pull cords” or “crime scores” that commercial insurers deem high-risk [13].

Financially, the benefits are clear. In some regions, traditional insurance premiums have skyrocketed by as much as 500% [12]. Group insurance models, however, offer more stable and predictable costs, allowing housing providers to focus their budgets on essential services and maintenance instead of absorbing steep premium increases. By keeping coverage affordable and consistent, these models help ensure tenant stability and long-term housing affordability.

Affordable housing providers are facing a tough reality: rising insurance premiums and shrinking coverage options. In this challenging landscape, government involvement becomes crucial. Public-private partnerships step in as a practical solution, combining the agility of private markets with the regulatory support of public policy. These partnerships aim to ensure affordable housing developments remain insurable, safeguarding homes for low-income tenants. The growing insurance market pressures have made these collaborations more important than ever.

In April 2024, New York State took a bold step to combat insurance discrimination. The Department of Financial Services enacted Insurance Law § 3462, which prohibits insurers from canceling policies, hiking premiums, or denying coverage based on a building's affordable housing status or tenants' use of Section 8 vouchers. This law followed a 2022 review that revealed 93% of property insurance applications (65 out of 70) asked landlords about tenant income or government assistance [6][14].

"Insurers... cannot inquire about on an application or cancel, refuse to issue, refuse to renew or increase the premium of a policy, or exclude, limit, restrict, or reduce coverage under a policy based on the fact that the real property being insured is an affordable housing development." - Bernard Ganley, Deputy Superintendent, Property Bureau, New York Department of Financial Services [6]

The stakes are high. Discriminatory practices have driven premiums up dramatically in recent years [14]. Governor Kathy Hochul highlighted the urgency: "Insurance discrimination drives up costs for property owners and renters and puts countless affordable homes at risk" [14].

In addition to regulatory protections, government-backed programs offer financial relief. During the COVID-19 pandemic, the U.S. Department of Housing and Urban Development (HUD) expanded the Emergency Solutions Grant (ESG) program under the CARES Act, dedicating $4 billion to prevent housing instability. HUD raised income eligibility limits from 30% to 50% of the Area Median Income and extended rapid rehousing assistance to curb potential mass displacement [5]. Programs like these act as safety nets, stepping in when economic shocks threaten housing security. These measures align with broader reforms aimed at stabilizing vulnerable housing markets.

The tightening insurance market has hit affordable housing providers particularly hard [6]. Unlike market-rate properties, Low-Income Housing Tax Credit (LIHTC) developments can't simply raise rents to offset soaring insurance costs, leaving them financially exposed [9].

To address this, states are introducing targeted reforms. Permanent tax credit exchange programs now allow developers to trade tax credits for direct subsidies when private investor demand declines during economic slumps [5]. Housing authorities are also using income recertification to adjust tenant rent contributions when individual incomes drop, helping to prevent evictions [5].

Research from Columbia Business School underscores the importance of public insurance models. While private insurers often focus on higher-income renters to maintain profitability, public programs can take on higher-risk households, mitigating the broader societal costs of homelessness [2][3]. This shared responsibility creates a more balanced system: private insurers handle stable markets, while public initiatives protect the most vulnerable. By spreading risk across both individual setbacks (like job loss) and broader economic downturns, these measures reduce barriers like large security deposits that often lock low-income tenants out of housing [2].

For housing providers, the takeaway is clear: stay informed about new regulations and take advantage of available protections. Laws like New York's Insurance Law § 3462 empower property owners to challenge unfair premium increases or coverage denials [6]. Additionally, state-backed entities like the New York Property Insurance Underwriting Association (NYPIUA) provide last-resort coverage options when private insurers fall short [6].

The eviction crisis in the U.S. remains a pressing issue. In 2024 alone, landlords filed over 1 million eviction cases in tracked jurisdictions, with a filing rate of 7.8% - roughly eight filings for every 100 renter households [15]. Phoenix, Arizona, set a staggering record with 86,946 filings, equating to one eviction filing every six minutes [15]. The financial toll of evictions affects both tenants and landlords, creating a ripple effect of economic strain.

This is where Rent Guarantee Insurance (RGI) steps in, offering a safety net for tenants during short-term financial crises caused by income loss or health emergencies [3]. Research from Columbia Business School highlights how RGI enhances financial stability by spreading risk across individuals and broader economic downturns. It also reduces the need for hefty security deposits, which often exclude low-income renters from accessing housing [2][3]. By ensuring rent payments continue during tough times, group insurance solutions like RGI help both tenants and landlords avoid the costly and disruptive eviction process.

Studies suggest that short-term rent support could prevent about 15% of potential displacements [4]. By bridging financial gaps caused by emergencies - like job loss, medical bills, or unexpected expenses - group insurance models keep families in their homes while ensuring landlords receive their payments. This approach not only mitigates the human and financial cost of evictions but also promotes long-term housing stability.

The benefits of group insurance and rent support programs are clearly visible in action. Programs like Keep King County Housed (KKCH), launched in July 2023, provide direct rent assistance and eviction prevention services to households facing nonpayment issues. Funded by the Washington State Department of Commerce and managed by United Way of King County, KKCH focuses on helping vulnerable tenants before they face displacement [17].

Cities with strong tenant protection policies have seen significant reductions in eviction rates. For example, Philadelphia and New York City implemented proactive housing stability programs that cut eviction filings to 52% of pre-pandemic levels [15]. By contrast, cities in the Sunbelt with weaker protections experienced record-high eviction filings. As researchers Sarah Johnson, Lorae Stojanovic, and Peter Hepburn observed:

"When cities take concrete steps to improve tenant protections, we see evictions decrease" [15].

Since 2018, over 100 guaranteed income pilot programs have been introduced across the U.S. Cities like Austin, Texas; Arlington, Virginia; and Chicago, Illinois, have tested direct cash support models to help renters stay housed [16]. According to the Urban Institute, cash-based approaches not only improve housing stability but also offer renters more choice and dignity while reducing discrimination against marginalized groups [16]. These programs are most effective when combined with insurance models that target households at the highest risk of eviction - particularly Black renters, who accounted for 36% of eviction filings despite making up only 28% of the renter population [15].

In 2022-2023, 29% of housing providers saw insurance premiums spike by 25% or more, while the share of cost-burdened renters rose to 50% [18][19]. These statistics highlight the challenges affordable housing communities face when trying to shield vulnerable tenants under traditional insurance models, which often lack the agility needed.

Walnut Insurance steps in with an embedded platform that seamlessly integrates rent and income protection into housing providers’ existing systems. Offering three levels of integration - Co-Branded Link Out (no setup required), Data-Driven Referral Link (light API configuration), and Headless API (full control) - Walnut removes technical barriers, making it easier for providers to adopt. This ease of implementation is crucial, as streamlined programs tend to attract more landlord participation compared to complex federal initiatives like Housing Choice Vouchers [1].

The Headless API stands out for large portfolio managers. It allows providers to maintain full control over their user interface while Walnut handles backend compliance and insurance processes. This setup reduces technical debt as providers scale and ensures that rent protection feels like a natural part of the tenant experience rather than an external service. By bridging the gap between traditional insurance limitations and the evolving needs of affordable housing providers, Walnut delivers a solution that’s both practical and effective.

Walnut connects housing providers with a network of over 14 insurance carriers, offering tailored solutions to combat rising premiums and rate hikes. This multi-carrier approach provides a safeguard against sudden cost increases that can occur when relying on a single provider.

The platform builds on established Rent Guarantee Insurance (RGI) concepts, offering partial rent payments to landlords when tenants face unexpected income losses or medical expenses [2][3]. Coverage options can be customized based on specific needs: private insurers often focus on higher-income renters, while public models aim to protect households most at risk of homelessness [2][3]. Studies show that short-term rent support can prevent about 15% of potential displacements [4], making Walnut’s customizable coverage a practical tool for maintaining housing stability amidst financial uncertainty.

Walnut’s approach goes beyond integration and customization to actively strengthen housing stability. By embedding rent and income protection into housing operations, Walnut creates a safety net for tenants during financial crises - times when eviction risks are at their highest. With homelessness rising 12% in 2023 to over 650,000 people [19], and insured losses from natural disasters increasing 40% over the past decade [18], the urgency for such solutions is clear.

Walnut’s instant quote and bind capabilities ensure rapid responses during tenant emergencies. This speed is critical in preventing evictions, as even a short delay can determine whether a family stays housed or faces displacement. Additionally, Walnut’s comprehensive compliance support and multi-channel broker assistance remove administrative obstacles, making it easier to scale protection. By enabling swift deployment and addressing income shocks head-on, Walnut plays a direct role in promoting housing stability and reducing eviction risks.

Group insurance models provide a practical way to prevent tenant displacement during financial hardships. Research consistently highlights how these programs significantly lower claim rates and reduce the risk of displacement, while also making housing more accessible to those who are most vulnerable.

These programs offer protection for both landlords and tenants by addressing risks on multiple levels. For landlords, they provide financial security, encouraging them to rent to individuals who might otherwise face barriers - such as those with credit issues or criminal records - groups that are statistically 10 times more likely to experience homelessness[1]. Tenants, on the other hand, gain a much-needed safety net during income disruptions or health crises. This eliminates the burden of large security deposits, which often stand in the way of securing housing. By pairing financial guarantees with case management and mediation, these models help resolve conflicts before they escalate into evictions.

The next step is integrating these effective models into digital platforms. Walnut Insurance takes this approach by embedding group insurance directly into existing housing systems. With connections to over 14 carriers, API-driven flexibility, and instant quote and binding capabilities, Walnut simplifies the process, removing technical and administrative hurdles that have slowed adoption in the past. As insurance premiums continue to rise, scalable solutions like these are crucial for ensuring housing stability in vulnerable communities.

Group insurance models, such as rent-guarantee or income-protection policies, play a crucial role in preventing evictions by stepping in to cover rent when tenants experience temporary income disruptions. Essentially, these policies transfer the financial burden from landlords to insurers, ensuring that rent is paid on time, even during short-term financial challenges. This provides tenants with a much-needed safety net, allowing them to stay in their homes while they work to regain financial stability.

For landlords, this setup offers peace of mind. By minimizing financial risk, these insurance programs make it easier for landlords to rent to tenants who might have less-than-ideal credit or irregular income. Research shows that these models can reduce eviction filings by as much as 30%, as landlords feel more confident about consistent rent payments. The result? Tenants are able to maintain their housing, while landlords avoid the costly and time-consuming eviction process - creating a win-win situation for both parties.

Captive insurance gives affordable housing providers a way to take control of their insurance needs by setting up their own insurance entity. This method turns unpredictable insurance costs into a steady and manageable budget item. Providers can customize coverage to address specific risks, such as floods, earthquakes, or tenant income loss. Unlike traditional insurance, captives help avoid sharp premium hikes and allow providers to keep surplus funds, which can then be used as savings.

By spreading risk across multiple properties, captives lessen the financial burden of individual loss events and provide a safety net during short-term income disruptions, such as tenants dealing with temporary unemployment. This stability helps providers keep rents affordable and steer clear of costly emergency measures. Captives also bring added benefits like better transparency, consistent pricing, and the flexibility to adjust coverage as property portfolios expand, ultimately supporting stronger, more stable housing communities.

Government involvement is a driving force behind the growth of group insurance models aimed at supporting affordable housing. Federal programs like HUD’s Housing Choice Voucher and Rental Assistance initiatives inject billions of dollars into the system, ensuring steady cash flow that insurers can leverage to create group policies. On top of that, resources like the Homeowner Assistance Fund, established through the American Rescue Plan, direct nearly $10 billion toward rent, mortgage, and utility relief. In some cases, states and cities are using these funds to help cover insurance premiums for tenants dealing with temporary income setbacks.

The government’s role goes beyond just funding. Agencies like HUD, along with nonprofit research groups, provide essential data on rent stability and loss prevention. This information helps insurers fine-tune their pricing models. There are also emerging policy ideas in play, such as integrating emergency rental assistance directly into federal housing programs, which could further reinforce these insurance frameworks. By blending public funding, regulatory backing, and data-driven approaches, government participation helps minimize financial risks, encourages broader adoption, and ensures tenants are better protected during tough times.