April 22, 2026

Missed payments hurt businesses. Whether it’s rent, utilities, or loans, late or unpaid bills disrupt cash flow, increase collection costs, and strain customer relationships. Bill protection programs solve this by ensuring steady payments during income disruptions, benefiting utility companies, landlords, and lenders.

Here’s how it works:

Utility companies face a persistent challenge with late payments. In 2022 alone, energy providers had to disconnect electricity for nearly 3 million customers who failed to settle their accounts [6]. Adding to this issue, over 56% of Americans struggle to pay essential monthly bills, underscoring the significant revenue risks these companies face [7].

One effective solution is offering bill protection programs that allow for incremental revenue collection through partial payments, which helps lower delinquency rates. For example, National Grid Massachusetts' Arrears Management Program and SoCalGas's 2021 AMP provide debt forgiveness while encouraging more consistent payments [3].

"Partial payments allow customers to contribute what they can, when they can, reducing stress and maintaining their access to critical services." – Steve Schult, InvoiceCloud

Flexible payment options like Apple Pay, Google Pay, and PayPal's "Pay in 4" not only make it easier for customers to pay but also ensure utilities receive funds promptly, reducing the risk of late payments [7]. These tools streamline cash flow without placing extra pressure on collection teams.

In addition to improving cash flow, these strategies help cut administrative costs. By reducing the need to chase overdue payments, handle high call volumes in customer service centers, or process service disconnections, utility companies can operate more efficiently [6][7]. It's worth noting that 68% of electric or dual-fuel budget billing customers use paperless billing, and 45% are enrolled in autopay [8]. These trends point toward a shift to more automated and predictable revenue streams, which can safeguard financial stability.

The success of these approaches in the utility sector provides a strong foundation for similar revenue protection strategies in industries like property management and lending.

Missed rent isn’t just an inconvenience - it disrupts cash flow and can make covering essential expenses like mortgages, taxes, and maintenance a struggle. Bill protection helps landlords shift from reacting to missed payments to proactively securing their income. Considering that tenant-caused damage and loss of rent make up about 50% of landlord insurance claims [9], protecting revenue becomes a critical component of property management.

Rent Guarantee Insurance (RGI) acts as a financial buffer for landlords. If tenants default on rent, RGI steps in to cover the missed payments after a 30-day waiting period. This coverage can last anywhere from a few months to a year, giving landlords a safety net while they navigate legal proceedings [10]. This is especially important in areas where eviction processes take longer. For example, in 2025, 17% of landlords cited compliance with new tenant protections and local regulations as a significant challenge [9].

"Missed rent is one of the fastest ways NOI gets disrupted. Even well-screened residents can run into job loss, medical issues, or other life events that make it difficult to keep up with payments." – Cosign

Modern property management systems make bill protection even more seamless by integrating it directly into rent collection workflows. Tools like real-time accounting synchronization prevent tenants from exploiting delays to make partial payments [22, 23]. Autopay features also play a big role here. Since payment history impacts 35% of a FICO® Score and 40% of a VantageScore® [11], enrolling tenants in autopay ensures rent is collected on time while also helping tenants maintain good credit.

The advantages go beyond avoiding rent defaults. Debt collection fees can eat up 25% to 50% of the recovered balance, and unpaid rent can affect a tenant’s credit for up to seven years [12]. By embedding bill protection into their systems, landlords can cut down on collection costs, preserve better relationships with tenants, and secure their revenue without the hassle of chasing payments. This approach mirrors strategies used by lenders to lower revenue risks and streamline operations.

Loan defaults tend to spike when borrowers, facing income disruptions, prioritize basic needs over loan payments. By Q4 2025, 12.7% of credit card users were 90 or more days past due, up from 11.35% the year before [16]. Similarly, auto loan delinquencies among households in low-income areas climbed by 70 basis points in Q3 2025 [14]. These trends highlight serious revenue risks for lenders - risks that bill protection can help address. While already a key tool in sectors like utilities and property management, bill protection is proving just as impactful for lenders.

Bill protection ensures that loan payments continue during periods of income disruption, offering critical support for borrowers with subprime (credit scores below 620) and near-prime (620–719) credit profiles [14]. With total U.S. credit card debt hitting a record $1.28 trillion in Q4 2025 [16], even small reductions in default rates can lead to significant revenue retention.

Modern lending platforms are integrating bill protection directly into loan origination processes through automated workflows. This allows borrowers to enroll effortlessly and ensures uninterrupted payments [13]. The seamless nature of these integrations reflects the growing importance of bill protection as a built-in feature, much like its role in utilities and property management.

The benefits of bill protection go well beyond preventing charge-offs. For instance, monthly auto loan payments surged nearly 30% between 2020 and 2023, driven by rising vehicle prices and interest rates [14]. By helping borrowers manage these higher payments, bill protection reduces the risk of account deterioration and protects lenders from losing revenue entirely [14]. With the overall consumer loan delinquency rate at 2.62% across commercial banks in Q4 2025 [15], even modest improvements in repayment rates can translate into measurable financial gains.

These integrations also enable tailored solutions for segments experiencing heightened delinquency rates. Loans originated between 2023 and 2025, for example, are showing higher delinquency rates compared to pre-pandemic loans. This underscores the value of embedding bill protection at the point of origination. Additionally, pairing bill protection with debt consolidation or refinancing options gives borrowers practical tools to handle high-interest debt while staying on track with their payments [16].

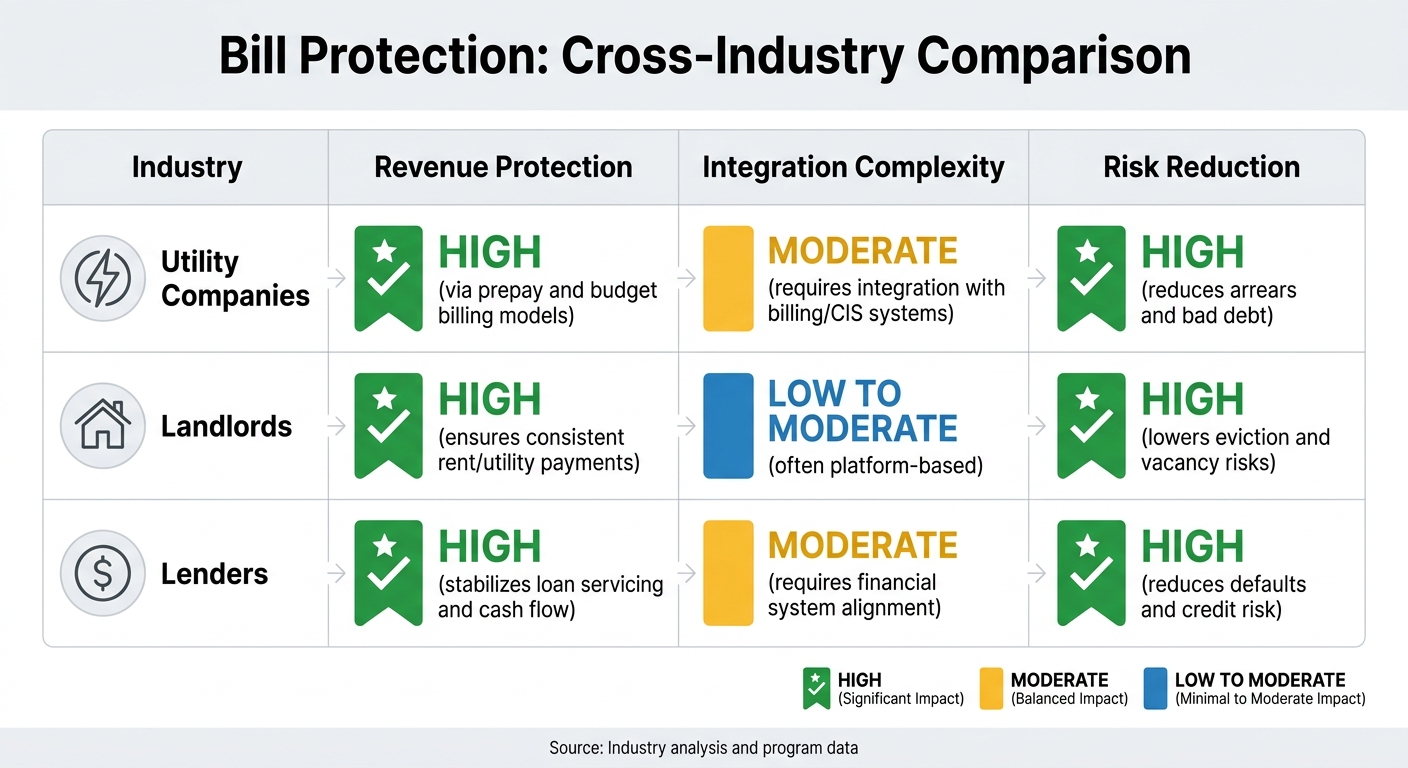

Bill protection delivers measurable benefits but comes with some trade-offs. For utility companies, it ensures strong revenue protection through prepay and budget billing models, which have shown household energy savings ranging from 5% to 14% [3]. However, integrating these programs can be moderately challenging, as it often requires coordination with existing billing systems and, in some cases, state agencies. Programs like Percentage-of-Income Payment Plans (PIPP), which cap energy bills at 6% of monthly income, are a prime example of this complexity [3].

Landlords benefit from consistent rent and utility payments with fewer integration hurdles, thanks to platform-based solutions. This consistency reduces the financial risks associated with evictions and vacant rental periods. For lenders, bill protection stabilizes loan servicing and cash flow, offering high revenue protection. However, they must ensure alignment with their financial systems to make these programs work effectively [5].

Here’s a snapshot of how these benefits and challenges compare across sectors:

Industry

Revenue Protection

Integration Complexity

Risk Reduction

High (via prepay and budget billing models)

Moderate (requires integration with billing/CIS systems)

High (reduces arrears and bad debt)

High (ensures consistent rent/utility payments)

Low to Moderate (often platform-based)

High (lowers eviction and vacancy risks)

High (stabilizes loan servicing and cash flow)

Moderate (requires financial system alignment)

High (reduces defaults and credit risk)

One notable challenge is the upfront system modifications required. Utilities, for example, need to adapt billing systems for arrears management programs, which often synchronize monthly payments with incremental debt forgiveness - sometimes reaching up to $2,000 per customer [3]. Lenders face their own hurdles, such as implementing robust API connections and fraud prevention mechanisms. Additionally, regulatory compliance adds to this complexity. The Federal Trade Commission (FTC) will enforce new "Total Price" disclosure requirements starting in May 2025, further increasing the need for compliance readiness [17][18].

Despite these challenges, the long-term benefits often outweigh the initial investment. Utilities that incorporate debt forgiveness programs strategically can maintain consistent future payments while ensuring that low-income households stay connected to essential services [3]. Similarly, lenders who integrate bill protection at the loan origination stage report noticeable improvements in repayment rates. These examples highlight how upfront investments can lead to stable, sustainable revenue across different sectors.

Bill protection ensures steady revenue streams for utilities, property managers, and lenders by addressing payment issues before they arise [3]. This makes early implementation a smart move.

As outlined earlier, introducing bill protection during critical moments - such as rising arrears or challenging economic conditions - shifts revenue management from being reactive to proactive [1][3]. Key triggers to watch for include arrears hitting critical thresholds, a 5% quarter-over-quarter increase in customer churn, or economic pressures affecting low- and moderate-income households.

The good news? Integration doesn’t mean overhauling your entire system. Start by pinpointing specific buyer triggers that align with your product’s strengths [1]. Use your CRM to maintain consistent, multi-channel communication with customers [4]. This approach not only simplifies operations but also enhances your overall B2B value offering.

"A strong B2B value proposition isn't just a tagline. It's a clear, customer-first statement of why your product solves a high-priority problem better than any alternative." - Stefan Maritz, Marketing Lead, CXL

To drive home the value, show tangible results - how bill protection reduces collections calls, prevents service disconnections, and cuts administrative expenses [2]. Clear communication of these benefits reinforces the key B2B advantages discussed throughout this article. Companies that excel in reducing risk and responding to customer needs achieve a 60% higher Net Promoter Score compared to those focusing solely on price [1].

Bill protection is a service designed to cover customers' bills when unexpected changes in their income or circumstances occur, providing them with much-needed financial stability. For utility companies, landlords, and lenders, this service helps minimize risks tied to revenue and collections. By integrating bill protection into billing platforms, service providers can ensure consistent revenue, strengthen customer loyalty, and offer a crucial safety net during periods of financial uncertainty.

Bill protection integrates directly into billing or loan platforms by connecting with automation and payment processing systems. These systems simplify tasks like invoicing, payment reconciliation, and sending customer notifications. They also incorporate secure payment methods and communication tools, enabling service providers to handle guaranteed payments effortlessly. This reduces manual work, improves collection efficiency, and boosts customer interaction - all within the platforms businesses already use.

Bill protection helps businesses handle the risk of unpaid bills. When customers experience income disruptions and are unable to pay, service providers or lenders often take on these costs. This approach reduces revenue losses while supporting customer retention and maintaining financial stability.