January 20, 2026

Embedded insurance succeeds where financial education struggles because it simplifies decision-making and removes barriers. While financial education assumes that knowledge changes behavior, embedded insurance integrates coverage directly into moments of need, making it easier for people to act.

Key insights:

Embedded insurance isn't just about convenience - it’s a smarter way to align with human behavior and ensure more people get the protection they need.

When it comes to insurance, the default option is often "no coverage", meaning consumers must actively choose to enroll. This seemingly small detail creates a significant barrier. Many people procrastinate or get stuck in a state of inertia, making enrollment less likely.

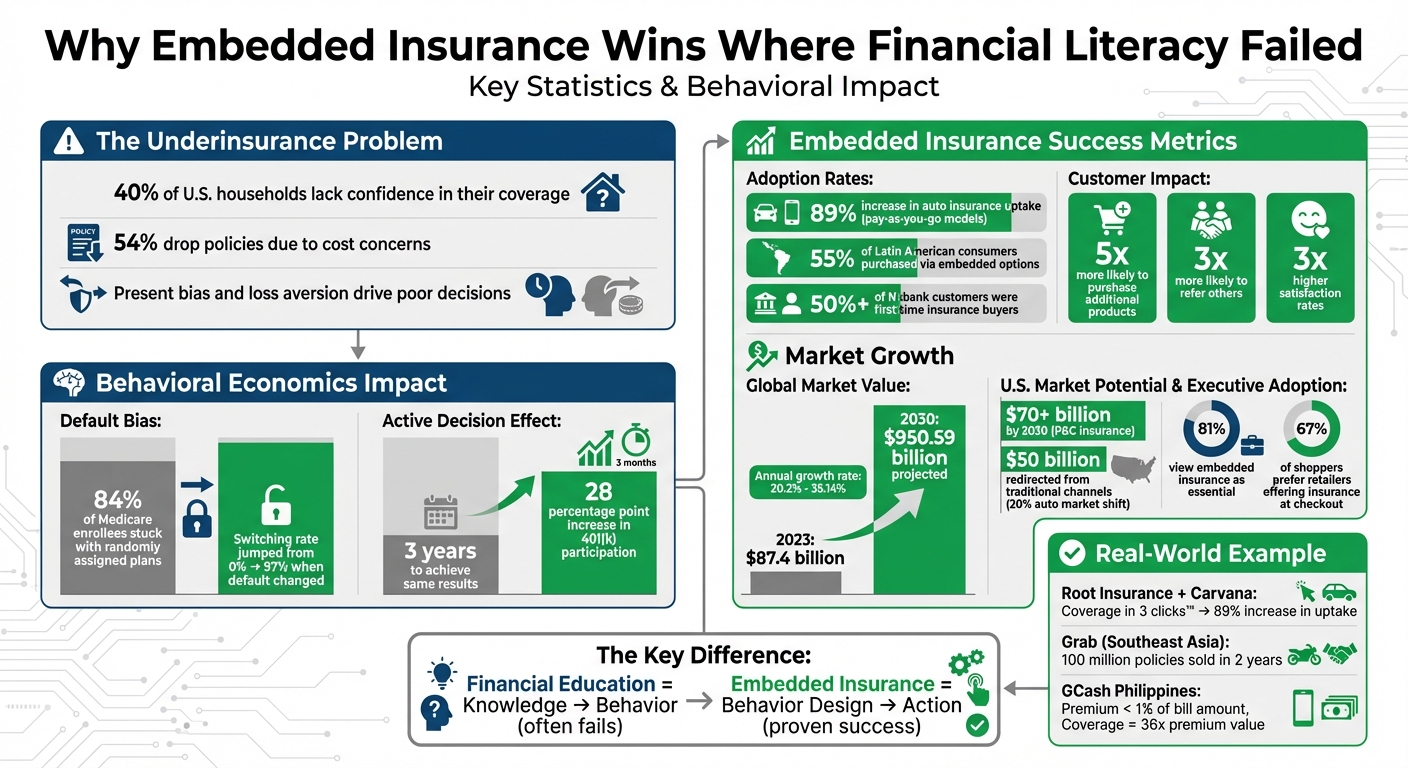

The influence of defaults is striking. For instance, a study on Medicare Part D beneficiaries found that 84% of new enrollees stuck with their randomly assigned default plan instead of exploring other options [7]. When the default was changed from "stay in the current plan" to "switch to a new plan", the switching rate skyrocketed from nearly 0% to an astonishing 97% [7]. This demonstrates how a simple tweak in the default setting can drive people to take action.

Even when individuals acknowledge the importance of insurance, the process of comparing plans and enrolling can feel overwhelming. Studies show that requiring people to make an "active decision" - choosing between options instead of simply opting in - boosted initial participation in 401(k) plans by 28 percentage points [4].

These behavioral tendencies pave the way for understanding how other biases, like present bias, further complicate insurance decisions.

Present bias nudges people toward prioritizing short-term gains over long-term security [6]. For example, saving money on premiums today might feel more rewarding than protecting against potential losses in the future.

"Present Bias: People tend to prioritize immediate gratification over long-term benefits. This bias can influence decisions about insurance coverage, with individuals opting for lower premiums in the short term but risking inadequate protection in the future." – William Kramer, Head of AXIS Group Benefits

For households with tight budgets, this bias becomes even more pronounced. A scarcity mindset, often driven by income volatility, makes it harder to justify upfront costs like insurance premiums [1]. When faced with the choice between paying for everyday essentials like groceries or covering an insurance bill, immediate needs almost always win. This explains why 54% of people who dropped or replaced an insurance policy did so because they believed it was too expensive [1].

While present bias pushes people toward short-term savings, another factor - loss aversion - shapes how they evaluate risks.

Although most people dislike monetary losses, many still underinsure because the guaranteed cost of premiums feels more burdensome than the uncertain benefit of protection [6][9]. In other words, paying a premium now can seem worse than the relatively remote chance of facing a significant financial loss later.

This tendency is amplified by how people perceive risk. Consumers often underestimate both the likelihood and the potential severity of negative events, leading them to opt for minimal coverage or skip insurance altogether [6]. When insurance is presented in isolation rather than as part of a broader financial plan, individuals may overlook how it supports their long-term financial stability [5].

The key to addressing these biases isn't simply educating consumers about risk. Instead, it's about how insurance is framed. By tapping into behavioral principles like loss aversion, default bias, and present bias, insurers can encourage better decision-making. For example, framing insurance as protection against specific, tangible losses - such as the financial strain of an unexpected event - tends to resonate more than abstract promises of peace of mind [8]. This approach makes the benefits feel immediate and relevant, helping overcome the psychological barriers to adequate coverage.

Financial education programs often fall short because they place too much responsibility on consumers while offering minimal practical benefits. These programs operate under the assumption that more knowledge will lead to better decision-making, but understanding insurance takes significant mental effort and time - resources many consumers are unwilling or unable to spare [2].

The reality is that most people prioritize price over policy details. They frequently opt for the cheapest insurance option without bothering to read the fine print [10]. This behavior stems from the complexity of insurance products, which makes them intimidating and difficult to grasp.

"Ignorance about basic financial concepts can be linked to lack of retirement planning and lack of wealth."

Another major issue is timing. General insurance education, delivered months or even years before it's actually needed, is often forgotten by the time a real risk arises. For instance, someone learning about travel insurance today might not remember the details when booking a flight next year. This disconnect highlights the need for a more practical and immediate approach to insurance education - one that eliminates the need for consumers to become experts before making decisions.

Embedded insurance solves these challenges by integrating coverage directly into transactions. Instead of requiring consumers to research and purchase insurance separately, this model presents a simple yes-or-no choice at the exact moment they face a potential risk - like booking a flight or buying an expensive item [11].

"The gist of embedded insurance is that it's often an easy yes-or-no choice."

This approach leverages the trust consumers already have in the brands they use, even if they don't necessarily trust insurance companies. A great example is GCash in the Philippines, which introduced "GInsure Bill Protect" as an option when users paid their bills. The premium cost was less than 1% of the bill amount, yet the coverage offered benefits worth 36 times that payment in cases of accidental death or disablement [11]. The simplicity and timing of the offer made it an almost automatic decision for users.

Pay-as-you-go insurance models also demonstrate the power of this approach. For example, offering flexible payment options for auto insurance led to an 89% increase in uptake [1]. By making the cost manageable and the decision effortless, embedded insurance eliminates the need for consumers to wade through complex policy details.

"Embedded insurance... helps with financial literacy, since customers don't need to navigate complex policies to make smart choices. Brands are accountable for making sure the right cover is already in place."

This streamlined method not only simplifies the decision-making process but also drives significantly higher adoption rates.

The difference in effectiveness between embedded insurance and traditional education-based methods is striking. A study by Hewitt Associates found that requiring new hires to make an "active decision" about 401(k) enrollment boosted participation rates by 28 percentage points in just three months. This was a dramatic improvement compared to the three years it took traditional methods to achieve the same results [4]. The study underscores the power of default options, a cornerstone of the embedded insurance model.

"Active decisions are optimal when consumers have a strong propensity to procrastinate and savings preferences that are highly heterogeneous."

Real-world examples further highlight the success of embedded insurance. At Nubank in Brazil, over half of the customers who signed up for "Nubank Vida" and "Nubank Celular Seguro" were purchasing life and phone insurance for the first time [11]. By integrating these offerings into their banking app, Nubank reached underserved and unbanked populations who had never interacted with traditional insurance providers. This seamless process broke down barriers that education programs alone could not.

Additionally, studies show that financial illiteracy actually makes default-based insurance enrollment more effective than requiring consumers to make informed decisions [4]. This insight explains why 81% of financial executives predict that embedded insurance will shift from being a "nice-to-have" feature to an essential offering [11]. It provides immediate protection without relying on a consumer's financial expertise.

The impact is particularly evident in emerging markets. In Latin America, 55% of consumers have purchased insurance through an embedded option - more than any other region globally [11]. These markets are bypassing traditional insurance models in favor of integrated, digital-first solutions, proving that embedded insurance is not just effective but transformative.

Effective UX design for embedded insurance focuses on reducing friction and aligning with behavioral principles like customer inertia and risk perception. The goal? Make coverage accessible in three clicks or less.

This approach relies on a few key design strategies:

A great example of this is Grab, the Southeast Asian super-app, which partnered with ZA Tech between 2019 and 2021 to introduce micro-insurance for its drivers. One standout product was a pay-per-trip critical illness policy, with premiums automatically deducted from driver earnings. This seamless integration helped Grab sell over 100 million policies in just two years [13].

Lemonade took a different path with its "Policy 2.0", a streamlined insurance model tailored for mobile users. By using a chatbot for purchases and a claims system capable of processing payouts in just three seconds, Lemonade transformed the insurance experience into something simple and intuitive [12]. This highlights the power of modernized language and instant feedback to make insurance approachable, not intimidating.

While an easy-to-use interface is critical for adoption, scaling these programs requires navigating complex compliance landscapes.

Scaling embedded insurance often runs into a major hurdle: regulatory compliance. In the U.S., insurance regulations vary by state, requiring providers to secure licenses for each region they operate in [15]. This complexity can slow expansion or even halt it altogether.

To sidestep these challenges, many businesses partner with third-party licensed producers rather than becoming full-fledged carriers. This strategy speeds up market entry and lowers costs but limits how non-licensed partners can earn revenue - they rely on clickthrough, ad, or referral fees instead of traditional commissions [15].

The most successful programs adopt a shared-responsibility model, dividing compliance duties between the customer-facing business and the insurer. This includes managing data privacy, consumer complaints, and consent for personalized recommendations or AI-based underwriting [3][14].

A compliance-by-design approach weaves regulatory rules into the technical infrastructure. Secure APIs and cloud systems ensure data privacy while handling high transaction volumes. Standardized APIs also make it easier for partners to integrate tailored insurance workflows without needing to manage complex rules themselves [14].

For companies expanding across multiple states, setting up local operational hubs helps address varying state laws and privacy regulations [17]. Some regions, such as Canada and France, even offer "innovation sandboxes" where businesses can test embedded insurance products in controlled environments before a full-scale launch [16].

Embedded insurance delivers measurable financial benefits. It typically offers higher profit margins than traditional insurance due to significantly lower distribution costs [18]. In 2023, the global embedded insurance market was valued at $87.4 billion and is expected to grow at an annual rate of 20.2% through 2032 [18]. In the U.S., embedded property and casualty insurance sales alone could exceed $70 billion by 2030 [3][14].

The impact extends beyond profits. Customers who feel their financial institution supports their financial well-being - an aim of embedded insurance - are:

This creates a feedback loop where embedded insurance strengthens the broader customer relationship, not just the insurance component.

For non-insurance businesses, embedded programs unlock new revenue streams via commissions. For insurers, they offer access to underwriting opportunities in digital-first environments [18]. If just 20% of the U.S. personal auto insurance market transitions to embedded models by 2030, it could redirect $50 billion in premiums from traditional channels to embedded partners [3].

"Embedded insurance is no longer just an add-on; it is becoming a native function of next-generation insurance technology platforms."

To maximize these benefits, companies should focus on high-volume partnerships and leverage real-time data analytics for A/B testing on placements and messaging [14][18]. This ensures continuous improvement in conversion rates and amplifies the overall business impact, making embedded insurance a cornerstone of broader product strategies.

Traditional financial education often overwhelms consumers with unnecessary complexity, making it difficult for them to navigate policy terms or compare coverage options. Embedded insurance flips this script. By integrating coverage directly at the point of need, it removes decision hurdles and leverages behavioral design principles like default settings and contextual relevance to align with how people naturally make choices.

The numbers back this up. The global embedded insurance market is forecasted to hit $950.59 billion by 2030, with an impressive growth rate of 35.14% annually [20]. In the U.S. alone, property and casualty embedded insurance sales are expected to surpass $70 billion by the same year [3][14]. Behavioral insights reveal that 89% of drivers are more likely to buy auto insurance when offered pay-as-you-go options [1]. Additionally, customers who feel their financial institution genuinely supports their financial well-being are five times more likely to purchase additional products and report triple the satisfaction levels [1].

These trends highlight how embedded insurance not only bridges the underinsurance gap but also creates opportunities for businesses to integrate strategic, customer-focused products seamlessly.

To successfully implement embedded insurance, focus on meeting customers at key decision points - like buying a car, booking travel, or checking out online. Simplify the process by using pre-filled data, offering coverage in just a few clicks, and exploring models where protection is bundled into premium tiers at no extra cost. The goal is to make adoption effortless.

The market demand is clear: 81% of financial executives now see embedded insurance as essential to meeting consumer expectations [20], and 67% of shoppers are more likely to spend with online retailers that include insurance options at checkout [19]. But this strategy isn’t just about boosting insurance sales - it’s about building stronger, more meaningful connections with customers by addressing their needs at the perfect moment. By doing so, businesses can create lasting value and loyalty.

Embedded insurance addresses present bias by automatically including coverage at the moment of purchase. This removes the burden of making a separate decision later - something many people tend to put off or avoid entirely. With this seamless approach, consumers gain protection without having to take any additional steps.

It also taps into loss aversion by presenting coverage as a safeguard against potential financial setbacks rather than an optional add-on. This framing emphasizes the risks of going uninsured, making the benefits of coverage feel more immediate and persuasive. By aligning with these natural tendencies in human behavior, embedded insurance boosts adoption rates effectively.

Embedded insurance works because it makes the process hassle-free by automatically including coverage as part of a purchase. It becomes a default-on option, eliminating the need for customers to actively opt in. Research on human behavior shows that people tend to stick with default settings, and by embedding insurance, buyers skip extra steps like researching policies or filling out forms. This aligns with how people naturally make decisions, leading to much higher adoption rates compared to traditional opt-in methods.

Features like pre-selected options, smooth digital processes, and pay-as-you-go pricing make embedded insurance feel like an integral part of the product, not an add-on. This reduces barriers and builds trust - customers who know they’re financially protected tend to feel more satisfied, recommend the service to others, and are open to exploring related offerings. Unlike financial literacy programs that require time and effort, embedded insurance transforms good intentions into instant, effortless protection, offering real support when it’s needed most.

Businesses can improve the customer experience by incorporating insurance directly into the purchasing process as a built-in, transaction-linked feature. Instead of treating it as an optional add-on, this method ensures insurance is pre-selected during checkout, with a simple and clear opt-out option. This taps into behavioral economics, where default options tend to drive higher adoption rates by minimizing the effort required to make a decision.

To make this work seamlessly, businesses should rely on a flexible, API-driven platform that can instantly calculate and finalize policy pricing using real-time data like location, purchase value, or device type. The checkout process should remain effortless, with insurance details displayed in a straightforward and transparent manner. For example, show the cost in clear terms (e.g., "Add $19.99 protection for 30 days") and use progressive disclosure - presenting only the most critical information upfront while offering the option to view more details if needed.

By embedding insurance directly into the transaction process, businesses can boost policy adoption, improve the perception of convenience, and strengthen customer trust. At the same time, this approach helps optimize conversion rates and ensures compliance with U.S. data privacy regulations. The result? A smoother, more reliable, and customer-friendly purchasing experience.