January 21, 2026

Embedded travel insurance is changing how travelers handle disruptions like canceled flights, lost luggage, or delays. Unlike older systems that require lengthy forms and manual claims, embedded insurance integrates directly into your booking process and uses real-time data to provide automatic payouts. For example, if your flight is delayed by three hours, you could receive compensation instantly - no paperwork, no waiting.

Key takeaways:

Embedded insurance is expected to grow from $13 billion in 2025 to over $70 billion by 2030, driven by its simplicity and efficiency. It’s reshaping travel insurance into a service that works for both travelers and businesses.

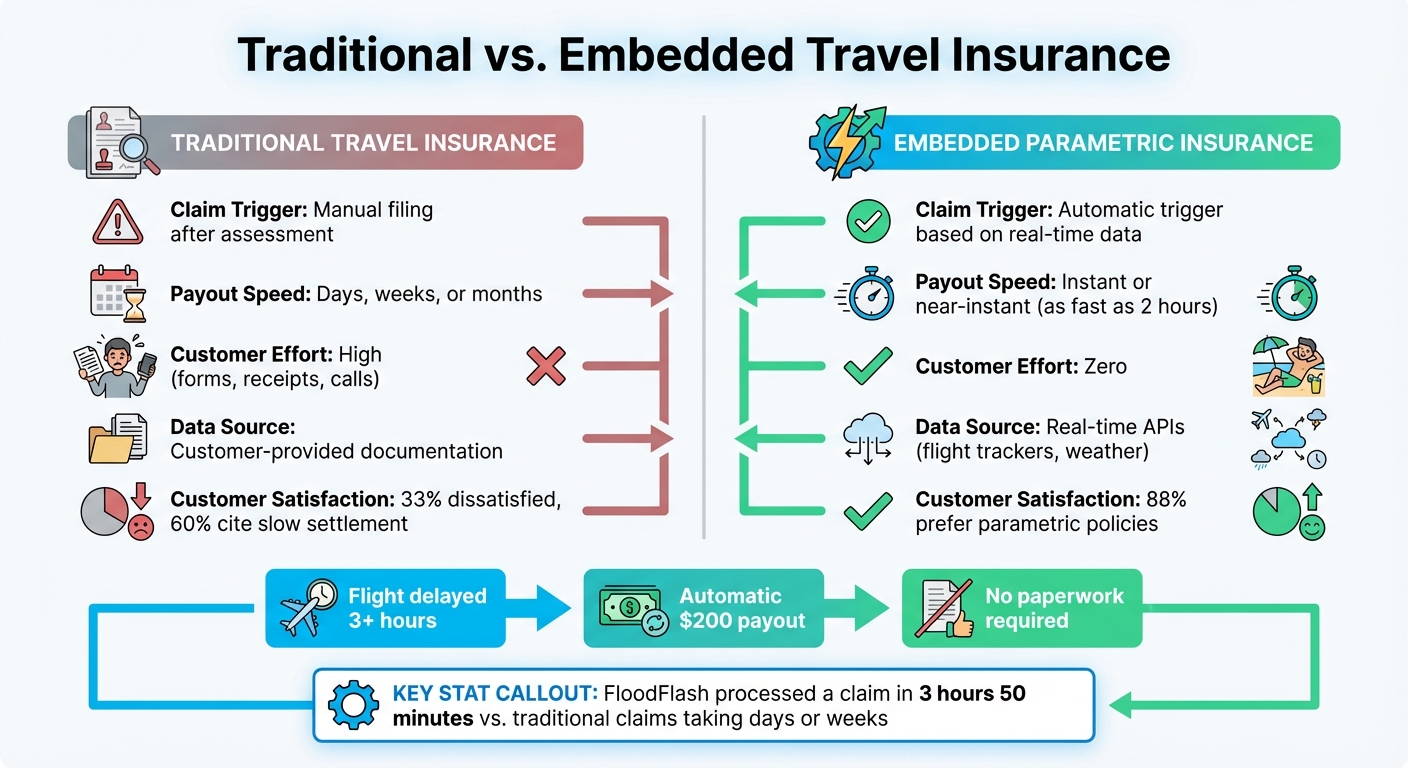

Traditional travel insurance often turns what should be a straightforward claim into a drawn-out ordeal. Imagine your flight gets canceled or your luggage disappears. Instead of quick assistance, you're faced with gathering piles of paperwork - receipts, forms, and reports. Then, a claims adjuster has to manually sift through every detail of your case.

The requirements aren’t just tedious; they’re rigid. Policies typically demand you notify all involved parties within 72 hours, even when you're scrambling to rebook flights or secure emergency accommodations. On top of that, you might encounter coverage rules that only kick in after delays of 6 to 12 hours, meaning you’re left covering meals or hotel stays out of pocket until then [3].

Behind the scenes, outdated IT systems make things worse. These legacy platforms, which lack modern APIs [2][4], funnel every claim into a slow, manual review process. The result? A clunky system that leaves customers frustrated and dissatisfied.

These inefficiencies have a direct impact on how customers feel about their insurance. A significant portion - one-third of claimants - report being unhappy with how their claims are handled. Of those, 60% point to the slow settlement process as their main gripe [3]. Claims that drag on for days or even weeks leave travelers stuck in limbo.

Adding insult to injury, fine-print exclusions often lead to disputes, further breaking down trust. For many, the hassle simply isn’t worth the effort. In fact, a large number of travelers skip filing claims altogether, knowing the process will likely take more time and energy than the payout justifies [3][5]. When insurance feels like more of a problem than a solution, it’s clear there’s a serious issue.

Embedded travel insurance takes a modern approach, replacing outdated, manual processes with a streamlined, automated system. Instead of dealing with cumbersome paperwork when something goes wrong, this system monitors your trip in real time and issues payments automatically when a covered event occurs. The entire process is powered by predefined triggers and APIs, making it fast and hassle-free.

Parametric insurance operates differently from traditional models - it pays out based on whether a specific event happens, not on the severity of the damage. As Walnut explains:

"Parametric insurance is a type of insurance that pays out a benefit based on the occurrence of a specific event, rather than the amount of damage or loss"

.

Here’s how it works: Imagine your flight is delayed by more than three hours. Real-time APIs track the delay and trigger an automatic payout as soon as the delay crosses the three-hour threshold specified in your policy. For example, $200 could be deposited directly into your account without you needing to file a claim, submit receipts, or wait for someone to review your case. These policies rely on objective, predefined parameters - such as flight delays or weather conditions - to ensure payouts are both fair and immediate [1].

Feature

Traditional Travel Insurance

Embedded Parametric Insurance

Manual filing after assessment

Automatic trigger based on data

Days, weeks, or months

Instant or near-instant

High (forms, receipts, calls)

Zero

Customer-provided documentation

Real-time APIs (flight trackers, weather)

APIs, or Application Programming Interfaces, are the technology driving embedded travel insurance. They connect booking platforms, insurance providers, and real-time data sources, allowing for instant policy issuance and claims processing [2] [4]. For example, when you book a flight, an API can immediately pull your trip details and offer insurance at checkout - no extra forms, no repetitive data entry.

This real-time data exchange eliminates the need for outdated batch-file systems, enabling thousands of transactions to be processed per second during busy travel periods [2]. APIs also support "headless" solutions, meaning travel companies can seamlessly integrate insurance options into their platforms while maintaining their branding and user experience. Meanwhile, the API handles all the heavy lifting in the background [2] [4]. This setup not only automates claims but also builds traveler confidence by cutting delays.

As Boston Consulting Group highlights:

"Embedded insurance is no longer just an add-on; it is becoming a native function of next-generation insurance technology platforms"

.

Embedded travel insurance offers a win-win scenario: it provides immediate relief for customers while opening up new revenue streams for businesses and significantly reducing operational expenses. By integrating this service directly into the purchase process, it tackles common pain points in claims handling head-on.

Speed matters. A staggering 60% of dissatisfied claimants cite slow settlement times as their main issue[3]. Embedded parametric models address this by triggering payouts instantly once a specific event is verified - no paperwork, no disputes.

Take FloodFlash, for example. In November 2022, this parametric insurer set a UK record by processing a claim in just 3 hours and 50 minutes after floodwaters hit the pre-agreed trigger depth[6]. While this example involves property insurance, the same technology is transforming travel insurance. It's no surprise that 88% of customers prefer parametric policies for their quick payouts[3].

Consider MAWDY, part of the MAPFRE Group. Partnering with Blink Parametric, they introduced flight disruption coverage between 2024 and 2025. Within 11 months, MAWDY saw an 11% increase in premium product adoption and a 21% rise in average policy premiums. Customers were given a choice: cash payouts or airport lounge access. Interestingly, 65% chose cash, while 35% opted for the lounge[3]. As Mark Seddon, CEO of Pact, puts it:

"The key is the lack of moral ambiguity. Neither those who determine the triggers, nor those claiming, can manipulate the triggers"

.

This transparency, powered by objective third-party data like flight statuses and weather reports, ensures a claims process that’s both fair and fast, building trust with travelers.

Beyond improving customer satisfaction, automation significantly reduces costs for insurers. Traditional claims processes - manual reviews, paperwork, and investigations - are time-consuming and expensive. Parametric insurance sidesteps these inefficiencies by using real-time data to automatically trigger payouts.

Maria Pavlenko, a tech journalist at AltexSoft, explains:

"Parametric insurance often involves lower costs for insurers. Since payouts are automatically triggered based on predefined conditions, the need for a traditional claims process - including claims adjusters, paperwork, and investigations - is eliminated"

.

Embedding insurance directly into booking systems further trims costs by eliminating the need for separate marketing efforts or additional sales staff. This streamlined approach contributes to higher margins. In 2023, the embedded insurance market reached $87.4 billion, with projections of a 20.2% annual growth rate through 2032[4]. Linking payouts to verified third-party data also minimizes the risk - and cost - of fraudulent claims.

Embedded insurance doesn’t just improve the claims experience - it’s also a financial boon for businesses.

This model creates new revenue streams through commissions or premium markups. In the agency model, businesses earn commissions on each policy sold without the hassle of managing payments or navigating complex regulations. The merchant model, on the other hand, allows businesses to set their own markups, though it requires handling additional technical and compliance responsibilities[3].

The potential revenue is substantial. Some online travel agencies now make more money from fintech add-ons, like disruption coverage, than from their core travel offerings[3]. By 2030, the embedded insurance market is expected to exceed $70 billion in gross written premiums, with some estimates pointing to a global opportunity of $3 trillion[2][7].

A great example is Sensible Weather, which sold 400,000 policies in 2024 by embedding weather-indexed coverage into 30% of theme park bookings and 10–15% of high-value accommodations[3]. This demonstrates how seamlessly embedded insurance can integrate into the customer journey.

Retention also gets a boost when customers see immediate value. Features like instant payouts or perks such as airport lounge access and hotel upgrades during disruptions foster loyalty. Insurtech expert Peter Dingle sums it up well:

"There are lots of things in the travel world where the marginal cost to deliver is very low, but have consumer value"

.

When customers feel protected and confident that claims will be handled quickly and fairly, they’re far more likely to return. This trust and transparency lay the foundation for lasting relationships.

Embedded travel insurance provides a variety of coverage options tailored to meet the diverse needs of travelers. From flight delays to lost luggage and unexpected cancellations, these solutions are designed to address the common risks that can disrupt travel plans.

Flight delays and cancellations are a reality for millions of travelers. In 2024 alone, about 236 million passengers in the U.S. experienced these disruptions - that’s roughly 1 in 4 flyers [3]. Trip cancellation and interruption coverage is a cornerstone of travel insurance, accounting for nearly two-thirds of travel insurance revenue in the U.S., with 89% of policies including this feature [8].

Embedded insurance takes this a step further by offering near-instant payouts. Instead of dealing with forms, receipts, and long waiting periods, travelers receive compensation automatically within just 2 hours. This is made possible through flight tracking APIs like FlightAware or OAG, which verify delays in real time. Depending on the policy, payouts are sent directly to your account or come in the form of perks, such as airport lounge access.

For example, a parametric flight delay policy might cost $20 and offer a $100 payout or lounge access if a flight is delayed by more than 2 hours [3]. This approach addresses smaller inconveniences that traditional insurance often overlooks, making travel disruptions less stressful.

Embedded insurance also steps in to protect your belongings and provide emergency assistance when needed.

Lost or delayed luggage is a common headache for travelers. In 2024, airlines mishandled 33.4 million bags worldwide, averaging 6.3 bags per 1,000 passengers [3]. Traditional claims processes often involve lengthy waits and tedious paperwork. With embedded baggage insurance, the process becomes much simpler. If your bag doesn’t arrive, you report it to the airline and receive a Property Irregularity Report (PIR) number. Entering this number into the embedded system triggers an immediate payout, often while you’re still at the airport. Using real-time tracking databases like SITA's WorldTracer, the system verifies the delay and credits your digital wallet or bank account, allowing you to buy essentials without delay.

In addition to baggage protection, embedded insurance provides 24/7 access to emergency services. This includes medical referrals, direct hospital billing, and even emergency evacuations when necessary [8][9].

For travelers seeking maximum flexibility, Cancel for Any Reason (CFAR) policies offer an appealing option. These policies allow you to cancel your trip for any reason, whether it’s a change of heart or concerns about safety.

CFAR policies typically reimburse 50% to 75% of your insured, prepaid, nonrefundable trip costs. However, they come with a few conditions: they must be purchased within 10 to 21 days of your initial trip deposit, and cancellations must occur at least 48 to 72 hours before departure [10].

Feature

Standard Cancellation

Cancel for Any Reason (CFAR)

Specific covered reasons (e.g., illness, injury)

Any reason

Up to 100% of nonrefundable costs

50% to 75% of nonrefundable costs

Up until departure

Within 10–21 days of initial trip deposit

Up to the moment of departure

At least 48–72 hours before departure

CFAR is typically offered as an add-on to comprehensive travel insurance plans. With embedded insurance, it’s seamlessly integrated into the booking process. This means travelers can easily add CFAR coverage with a single click during checkout, providing an extra layer of peace of mind.

After understanding the impact of embedded travel insurance, businesses can take concrete steps to implement it. There are three main methods to integrate embedded insurance, each tailored to different levels of technical capability and customization. The key is selecting the approach that matches your business goals and resources.

This is the easiest way to get started with embedded insurance, requiring no technical setup. Your business directs customers to a co-branded insurance portal, where they can purchase coverage. You can customize basic branding elements, but the insurance provider manages everything else, including quotes and policy issuance.

The downside? Limited customization. Since customer data isn’t shared, travelers must manually enter their trip details, creating a small extra step. However, this is still far more convenient than having customers search for insurance independently. For businesses with limited technical resources or those testing the waters, co-branded link-outs offer a fast, low-effort way to generate revenue.

This option is a step up in terms of integration. By using minimal API connections, your platform can share trip details with the insurance provider. For example, when a customer books a flight or hotel, their travel information is automatically transferred to the insurance quote form, making the process seamless.

This smoother experience often leads to higher conversion rates. Customers appreciate the convenience, and businesses gain access to valuable analytics. You can track which routes or customer segments are most likely to purchase insurance, helping refine your offerings. While this method requires some technical setup, it strikes a balance between ease of implementation and improved customer experience.

For businesses aiming for full control, headless API integration is the most advanced option. This approach embeds the insurance process directly into your platform, allowing customers to complete everything - from selecting coverage to purchasing - without leaving your site. It can be seamlessly integrated into your checkout flow or mobile app.

Although this requires a higher level of technical expertise, it offers unmatched flexibility. You control the user interface, ensuring the insurance offering aligns perfectly with your brand. Real-time APIs handle risk management, pricing, and policy issuance instantly. For parametric products, like flight delay coverage, these APIs can trigger automatic payouts as soon as a delay is confirmed - eliminating the need for customers to file claims.

"Embedded insurance is no longer just an add-on; it is becoming a native function of next-generation insurance technology platforms." - BCG

The market for embedded insurance is expected to grow from around $13 billion in 2025 to over $70 billion in gross written premiums by 2030 [2]. Businesses that adopt deeper integration now are better positioned to capture a share of this booming market while meeting travelers' expectations for fast, seamless service.

Embedded travel insurance is reshaping how coverage works by swapping out manual claims for automated systems powered by parametric models and autonomous AI. These advanced systems handle everything - from underwriting to payouts - without needing human involvement. For instance, if a flight is delayed by more than three hours, travelers get instant notifications and automatic compensation, no paperwork required [2][11]. This shift is setting the stage for faster, more efficient travel insurance solutions.

These immediate payouts are proving to be a game changer. Companies offering parametric flight delay solutions often see a 5–10% boost in total sales and a 21% jump in average policy premiums within just 11 months of rolling them out [3].

The technology driving these changes is evolving at a rapid pace. Autonomous AI systems are now capable of handling multi-step processes, making claims handling faster and more accurate [2]. Meanwhile, cloud-native infrastructures process thousands of transactions every second, paving the way for micro-policies that can cover specific parts of a journey [2].

For travel businesses, this technological leap offers a chance to meet growing customer demands for instant, hassle-free service while unlocking fresh revenue streams. The future of travel insurance lies in its ability to integrate seamlessly into every travel experience, boosting efficiency and building stronger customer trust.

Embedded travel insurance takes the hassle out of claims by relying on data-driven triggers rather than traditional paperwork. When you book a trip, the policy is automatically tailored to your itinerary and clearly outlines payout conditions - like a flight delay of 2 hours or more, a cancellation, or a missed connection.

Here’s how it works: real-time data, such as updates from airlines or airports, is used to detect when a trigger condition is met. Once that happens, the system calculates the payout instantly and transfers the funds directly to your account. No forms, no receipts, no back-and-forth emails. This streamlined process not only ensures travelers are compensated quickly and without stress but also helps insurers cut costs.

Parametric models are changing the game for travel insurance by streamlining the entire process. Here's how it works: when a specific event, like a flight delay of 2 hours or a cancellation, is verified through reliable data sources, the payout is triggered automatically. Since the payout amount is pre-determined, there’s no need for drawn-out claims processes or detailed evaluations of losses. This makes parametric insurance easier to navigate and often more budget-friendly compared to traditional options.

One of the standout features is instant payouts. Once the event is confirmed, funds are sent to travelers within minutes - no paperwork, no phone calls. This quick response provides immediate financial support for unexpected expenses like meals or hotel stays. On the flip side, insurers benefit too, with lower administrative costs and stronger safeguards against fraud. It’s a win-win setup that simplifies life for both travelers and insurance providers.

Businesses can seamlessly incorporate travel insurance into their platforms using Walnut's versatile tools. They can opt for co-branded links for a quick setup, no-code widgets that autofill traveler details, or dive deeper with a customizable API for tailored integration. Once customers enter trip details like dates and destinations, Walnut’s system instantly provides personalized policy options with pricing.

One standout feature is the use of parametric insurance. This leverages real-time data - like flight delays or cancellations - to trigger automatic payouts, eliminating the hassle of forms or manual claims. Additionally, Walnut’s platform offers an intuitive dashboard where businesses can tweak coverage limits, pricing, and event triggers. This not only creates a smooth experience for travelers but also helps businesses cut costs and boost customer satisfaction.